Have you ever wondered how much money is required for you to achieve independence?

Max also faced the same problem when drawing up his Masterplan to retire by 40.

Not knowing the size of your retirement gold nest is akin to running a race without knowing the finishing line. You cannot plan for it and spread your resources, and most importantly, you will forever be in the race.

In this post, I am going to share my personal guideline on the retirement savings required for financial independence. You may be surprised that the amount required may not be as much as you thought. But first, let's discuss some of the guidelines others are advocating.

The Million dollar question, literally

For some of us who are not so financially literate, a nice whole number of $1 million seems to be a financial goal reasonable enough to strive towards, but $1 million 10 years down the road will be much less valuable than today.Depending on your desired retirement lifestyle and time value of money, majority will soon find themselves falling into one of the two circumstances:

- Retirement money is unable to sustain retirement lifestyle - this is the group of people who retired after saving up $1 million, only to find that their retirement money is insufficient for their old age.

- Could have retired earlier - this is a good problem by failing on the safe side. But for people seeking early retirement to .... (insert all your wonderful reasons for wanting to achieve early financial independence here)..., this is likely not going to be a good way to base our retirement milestone upon.

|

| The two likely circumstances of saving $1 million for retirement |

The point is, there is no one size fits all number when it comes to retirement planning. $1 million may be more than sufficient for someone, but a far shot from what is required for another.

Save up 8 times your salary, they say

What really tickled my mind (and myself) is when I came across articles suggesting that we should have 8 times our ending salary when we retire at 67.

By disregarding spending lifestyle, this implies that two same-salaried person can retire with the same amount of money, even though one may lead a significantly more frugal lifestyle than the other.

By disregarding spending lifestyle, this implies that two same-salaried person can retire with the same amount of money, even though one may lead a significantly more frugal lifestyle than the other.

For someone spending $80k per year out of a $100k annual income, it is hard to imagine the consequences if he declare financial independence with only $800k (8 times of his annual income) saved up. That is unless if he expects an exceptionally high annual returns on his retirement money.

It should be quite obvious by now to realize that we cannot disregard annual spending in the discussion of retirement savings.

Another common way is to multiply your annual expenses by 25 based on the 4% safe withdrawal rate (SWR).$800k will only last 13 years with annual spending of $80k

Based on inflation rate of 3% and ROI of 7%, a quick calculation will show that a savings of $800k will only sustain 13 retirement years with an annual spending of $80k.$800k will last 20 years with annual spending of $60k

If the annual spending is reduced from $80k to $60k, the savings will then be able to last 20 years, which is a more realistic period for a 67 years old retiree.It should be quite obvious by now to realize that we cannot disregard annual spending in the discussion of retirement savings.

25 times of annual expenses, that's more like it

This is based on the assumptions that our portfolio can generate an annual returns of 7%, an average inflation rate of 3%, and we want our retirement money to last forever.

Max finds that this method is neat, simple to understand, and most importantly, makes financial sense.

For a different annual return on investment, we can simply multiple our annual expenses by a different number, easily derived from the inverse of the new SWR.

For example, if our annual expenses is about $80k, then we will need to have $2 million (25 times of annual expenses) in my retirement portfolio. At 7% ROI, the portfolio will be able to generate $140k in annual income, of which $80k will be used for expenses that year, and the remaining will be added to the retirement portfolio to generate a higher income next year, to account for inflation.

When the safe withdrawal rate method 'fails'

One big underlying assumption in using the safe withdrawal rate method is that the principle amount in your retirement money should never run out. In fact it should keep increasing yearly to counter inflation.This may be a reasonable approach to estimate our retirement savings required, but the SWR method will result in unrealistically huge retirement savings for people with low (or close to zero) ROI.

In fact, the SWR method cannot be applied if the ROI is lower than the inflation rate - the retirement savings required will be infinity. Even if the ROI is slightly higher than the inflation rate by, let's say 1%, the SWR method will recommend a retirement savings at 100! times the annual spending.

Retirement savings required should vary according to years of retirement living

One important factor that will affect the size of the retirement savings required is the expected years of living after retirement. Of course, we can always use the SWR method and ensure that the savings will never run out. But this will require a much larger pool of savings, which will directly translate to a much later retirement age.

Table below summarizes the three recommended retirement savings discussed earlier. Let's ask ourselves this question: What would you do if you are 40 years old, wants to retire as early as possible, and have saved up $1 million for retirement?

|

| Three different method recommends three different retirement savings requirement - which one to follow? |

Definitely retiring now is not an option unless you expects your life to end in no more than 18 years (touch wood). At 40 years old, this is quite unlikely.

A safer plan would be to work another 20 years to double the retirement savings to $2 million, which by then you would be 60 years old, almost too late to live the retirement lifestyle you have always wanted to.

Or, you can find out the amount required that can sustain another 50 years of your desired retirement lifestyle, assuming you expect to live up to 90. We know that this amount will be between $1 million to $2 million.

What if now instead you are 70 years old, and have similarly saved up $1 million for retirement. In this cases, unless you are looking to leave behind huge bequest eventually, immediate retirement will be a more likely option.

The four key factors that determines your retirement savings

Now should be a good time to put everything together: The amount of retirement savings required should be dependent on four key factors

- Annual expenses (affected by retirement lifestyle)

- Return on investment of retirement savings

- Expected years of living after retirement (affected by life expectancy and retirement age)

- Inflation rate

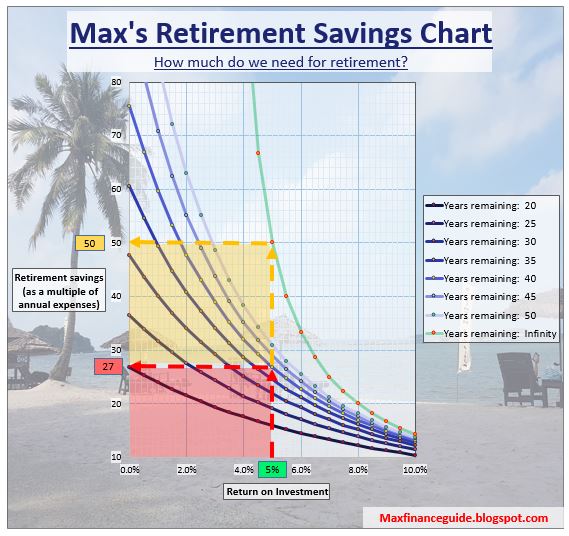

Max's Retirement Savings Chart

The retirement savings chart is designed for anyone who wish to find out their required retirement savings to be financial independent, without the use of online calculators or complicated formulas.

The main difference between the Retirement Savings Chart and the SWR method is the consideration of years of retirement living. By ensuring that the retirement savings does not run out forever, the SWR is assuming an infinite years of retirement living.

Here are some necessary assumptions used in

The main difference between the Retirement Savings Chart and the SWR method is the consideration of years of retirement living. By ensuring that the retirement savings does not run out forever, the SWR is assuming an infinite years of retirement living.

Here are some necessary assumptions used in

- Annual inflation rate of 3%

- Base annual expenses in retirement to remain unchanged, except for increment due to inflation

- Retirement savings will slowly decrease and be depleted by end of remaining years

For example, Alfred is now 40 years old, plans to retire by 50 years old, and he wants his savings to sustain another 40 years of his life until he is 90 years old. He intend to invest his retirement savings in fixed deposits and bonds which gives him a returns of about 5% per annum. Alfred estimates that he needs about $50k per year in today's dollar for his retirement lifestyle. This is equivalent to $67.2k per year based on 3% inflation rate for 10 years (between his retirement age of 50 and current age of 40).

Based on the SWR method (the green line), Alfred need to save up 50 times his annual expenses, or a whooping $3.36 million (50 x $67.2k) to ensure that his savings will never deplete.

However, if Alfred wish to find out the minimum amount of savings to finance his retirement for just his remaining 40 years, the Retirement Savings Chart shows that he only needs to save up 27 times his annual expenses, or $1.82 million (27 x $67.2k).

Don't get me wrong, I don't mean to imply that $1.82 million is a small sum, but for advocates of early retirement, this is definitely a much achievable amount than $3.36 million using the SWR method.

|

| Retirement savings required based on 5% ROI, 3% inflation rate and 40 remaining years |

Ending Note

Knowing how much we need in retirement savings is the first important step in planning for early financial independence. Max needs to save up about 30 times of his annual expenses before he can say goodbye to his day job. What about you?

----------

MAFIA

----------

----------

Similar posts

CPF Retirement Sum Scheme | Can I achieve the CPF retirement sum when I reach 55?

Financial Independent Model | Find out your retirement age now

Do you have a plan for early retirement?

Financial Independent Model | Find out your retirement age now

Do you have a plan for early retirement?

Images for happy new year whatsapp status

ReplyDeleteThis comment has been removed by the author.

ReplyDeleteThis comment has been removed by the author.

ReplyDeleteزينب زيادة

ReplyDeleteزينب زيادة

zianab zyada

تعتبر شركة الدرع المثالي من افضل شركات الخدمات فى المملكة العربية السعودية وتقدم العديد من الخدمات مثل شركة تعقيم بالرياض بالاضافة الى شركة تعقيم بجدة و شركة تعقيم بالدمام و شركة تعقيم بالقصيم بفضل جودة الخدمات التى تقدمها الشركة دائما تحصل على تقيم اعلى مما جعلها من اكثر الشركات ثقة لعملائها

ReplyDeleteالحجر الهاشمي

ReplyDeleteطريقة تركيب الحجر الهاشمى

سعر متر الحجر الهاشمى توريد وتركيب

اسعار الحجر الهاشمى

Money making blog I would like to say that this blog really convinced me to do it! Thanks, very good post.

ReplyDeleteBlogg Wow, cool post. I'd like to write like this too - taking time and real hard work to make a great article... but I put things off too much and never seem to get started. Thanks though.

ReplyDeleteThe luxurious feel of carpets from Dubai adds warmth and elegance to any home decor.

ReplyDelete