Followers of this financial blog would know that Max has been working on the Financial Independence Model (FIM) since the beginning of 2017. In a nutshell, the FIM is designed to help individuals compute their personalized FI age, based on basic financial information provided by the user.

For readers who are new to the FIM, a more detailed post on the main functions and principle of the model can be found in the post here.

So far, Max has tested the model with financial input from over 10 readers, with reasonable and logical output achieved. Below is the feedback from one reader who has found the model useful. It gives myself a great sense of satisfaction to develop a fully functional model that is useful.

However, as with all models in the world, the FIM output is computed based on a pre-defined set of formulas and rules. To be confident that the financial output is applicable to yourself, it is important to understand the modelling rules and assumptions of the FIM.

In this post, Max will describe in deeper details on the modeling principle of the FIM.

In this post, Max will describe in deeper details on the modeling principle of the FIM.

*Note: Input for the FIM is identified in blue for the remainder of this post

Objective of FIM

There are a few simple formulas out there we can use to compute our FI age. One popular method can be found here from Mr. Money Mustache, which states that the years to reach retirement is dependent on your saving rate as a percentage of your take-home pay.

This quick calculation by Mr. Money Mustache is very useful for anyone who wish to have a rough sensing of their years to retirement, but may not be ideal for someone who wish to plan out their retirement road-map in more details.

This is also the fundamental reason why Max decides to develop the FIM. Afterall, our retirement road-map should be unique to ourselves to be executable and achievable.

Objective of the FIM: Compute minimum retirement age based on customized financial input, with in built financial principles in Singapore's context.

Principle of the FIM

The overall flow of the FIM modelling rules is pretty straightforward, but may take some time to digest.

In brief, the model takes in all the expected income and spread them across the various baskets of cash equivalents after accounting for expected expenses and CPF contribution.

Upon FI age, the cash equivalent will be drawn upon to sustain the retirement life, which will be supplemented by the CPF savings at the later stage of our retirement.

The basic principle is to ensure that the pool of savings accumulated is sufficient to sustain the retirement lifestyle until the last age (to be determined by user), as compared to letting the savings last forever, which is practically impossible due to inflation.

|

| FIM modeling principle |

Income and expenses

The income and expenses are one of the most critical input to the FIM. Someone who expects zero expenses for the rest of his life can in fact retire yesterday. On the other hand, someone who has a higher annual expenses than annual income can forget about retirement altogether.

Expected income:

- Employment income - determined by monthly gross income and annual bonus, which will be increased yearly based on the annual increment rate, with annual contribution until the age of FI.

- Additional income - which user can input to capture one-off income at specific year, or repeated supplementary income that has a corresponding time validity.

Expected expenses:

- Basic/ survival expenses - are regular and recurring in nature, which will be increased based on inflation rate. Basic annual expense has no time frame, and will continue indefinitely until end of modeling age.

- Additional expenses - similar in concept to additional income

The income and expenses are one of the most critical input to the FIM. Someone who expects zero expenses for the rest of his life can in fact retire yesterday. On the other hand, someone who has a higher annual expenses than annual income can forget about retirement altogether.

Expected income:

- Employment income - determined by monthly gross income and annual bonus, which will be increased yearly based on the annual increment rate, with annual contribution until the age of FI.

- Additional income - which user can input to capture one-off income at specific year, or repeated supplementary income that has a corresponding time validity.

Expected expenses:

- Basic/ survival expenses - are regular and recurring in nature, which will be increased based on inflation rate. Basic annual expense has no time frame, and will continue indefinitely until end of modeling age.

- Additional expenses - similar in concept to additional income

|

| Additional income/ expense table for user to customize their income/ expenses |

Allocation of cash equivalent

The two main categories in the model are cash equivalent and CPF savings, which are the two main form of savings to support our retirement plans.

Cash equivalent are further grouped into the following baskets:

- Emergency fund - to be maintained at percentage of annual basic expenses earning risk-free interest rate. E-fund will be set to zero after age to stop maintaining E-fund (which is usually the FI age).

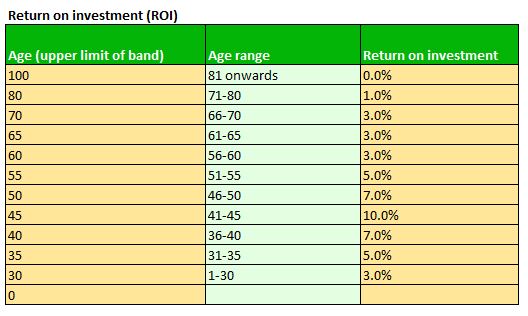

- Investment (cash) - investments that can be converted to cash to finance expenses when necessary, earning profit based on ROI table.

- Investment (SRS) - investments using savings in SRS, earning profit based on ROI table. The combined investment in cash and SRS will be maintained at percentage of 'investible' fund, to be cap at maximum investment sum.

- Savings - remainder of cash equivalent that is not kept as E-fund or invested, earning basic interest rate.

Relationship between the investment (cash) and investment (SRS) will be elaborated in another post.

The allocation of cash equivalent to the various baskets can be easily customized to match individual's financial preference, risk tolerance and investment proficiency. This can be seen from the large number of variables that can be adjusted by users.

For example, the ROI table below allows user to set different ROI at different age range.

Non investment savvy people can also set the percentage of 'investible' fund to zero, to allocate all the cash to savings.

|

| ROI table for user to customize their investment profit |

CPF savings and schemes

CPF is the other main category of saving for the model, which is why the FIM is very applicable in our local context. The CPF is an integral part to our retirement, so the FIM will not be complete without building in the CPF concept.

Interest earned from each of the accounts is also modeled based on the CPF interest rates, which also include the extra interest and additional extra interest for eligible CPF savings. More details is available on the CPF website here.

CPF allocation rate, extracted from CPF website

Users can also decide whether to maintain their CPF at the full retirement sum (FRS) or the enhanced retirement sum (ERS) at age 55.

In general, the sum keep in CPF RA account will earn an annualized rate of return of about 5% to 5.5%, so if your ROI is below this range, the better option will be to keep the CPF savings at ERS.

The estimated annualized rate of return for CPF RA savings will be elaborated in another post

CPF savings and schemes

CPF is the other main category of saving for the model, which is why the FIM is very applicable in our local context. The CPF is an integral part to our retirement, so the FIM will not be complete without building in the CPF concept.

Interest earned from each of the accounts is also modeled based on the CPF interest rates, which also include the extra interest and additional extra interest for eligible CPF savings. More details is available on the CPF website here.

|

| CPF allocation rate, extracted from CPF website |

Users can also decide whether to maintain their CPF at the full retirement sum (FRS) or the enhanced retirement sum (ERS) at age 55.

In general, the sum keep in CPF RA account will earn an annualized rate of return of about 5% to 5.5%, so if your ROI is below this range, the better option will be to keep the CPF savings at ERS.

The estimated annualized rate of return for CPF RA savings will be elaborated in another post

As the ERS and FRS in the future will be much higher than the amount today ($166k and $249k as of Jan 2017), the FIM has an in-built function to extrapolate the estimated FRS and ERS amounts at user's 55 year of age, based on the historical rate of increase for the past 15 years.

Any withdrawal from CPF savings at age 55 and CPF LIFE payment at age 65 will be contributed towards the cash equivalent pool.

Another key usage of the CPF is the public housing scheme (PHS). User can input their own BTO-related variables such as the downpayment sum and the BTO monthly installment (using CPF OA) to determine the utilization of the CPF OA account towards housing.

As the ERS and FRS in the future will be much higher than the amount today ($166k and $249k as of Jan 2017), the FIM has an in-built function to extrapolate the estimated FRS and ERS amounts at user's 55 year of age, based on the historical rate of increase for the past 15 years.

Any withdrawal from CPF savings at age 55 and CPF LIFE payment at age 65 will be contributed towards the cash equivalent pool.

Another key usage of the CPF is the public housing scheme (PHS). User can input their own BTO-related variables such as the downpayment sum and the BTO monthly installment (using CPF OA) to determine the utilization of the CPF OA account towards housing.

Initialization of FIM

The model requires a 'start state' to commence modelling, so users are required to provide their financial status for their current age. These include the

- current cash equivalent,

- current CPF balance (in each of the OA, SA and Medisave accounts),

- current annual gross income and expenses, and

- current SRS balance

Testing out the FIM

I have created a sample input here for Imaginary Joe, whom based on the FIM output, can retire in 7 years' time using a hypothetical financial input.

If anyone would like to receive their customized output using the FIM, please feel free to contact Max using the contact form here.

Sharing is caring, isn't it.

If anyone would like to receive their customized output using the FIM, please feel free to contact Max using the contact form here.

Sharing is caring, isn't it.

To be continued on part 2...

----------

MAFIA

----------

----------

No comments:

Post a Comment